Management Consolidation 101

Management consolidation, also known as segment consolidation, focuses on presenting aggregated financial results by the organization’s strategic business groups such as geographical location, business divisions, products, services, and brands.

At times, management consolidation leverages statutory consolidation, but it can also be an entirely separate process. Management consolidation is prepared separately to provide users with a different perspective on the companies’ performance.

Unlike legal or statutory consolidation which presents entity-level and group-level performance, management consolidation provides a deeper understanding of your business performance by strategic segments, with a level of detail that will be important for decision making and controlling purposes.

In this article, we will be discussing what it takes to get started on management consolidation, how to avoid common pitfalls and how you can set up organizational structures that are meaningful to your business.

Table of contents

How to get started on management consolidation? What should you take note of?

Organizational structure

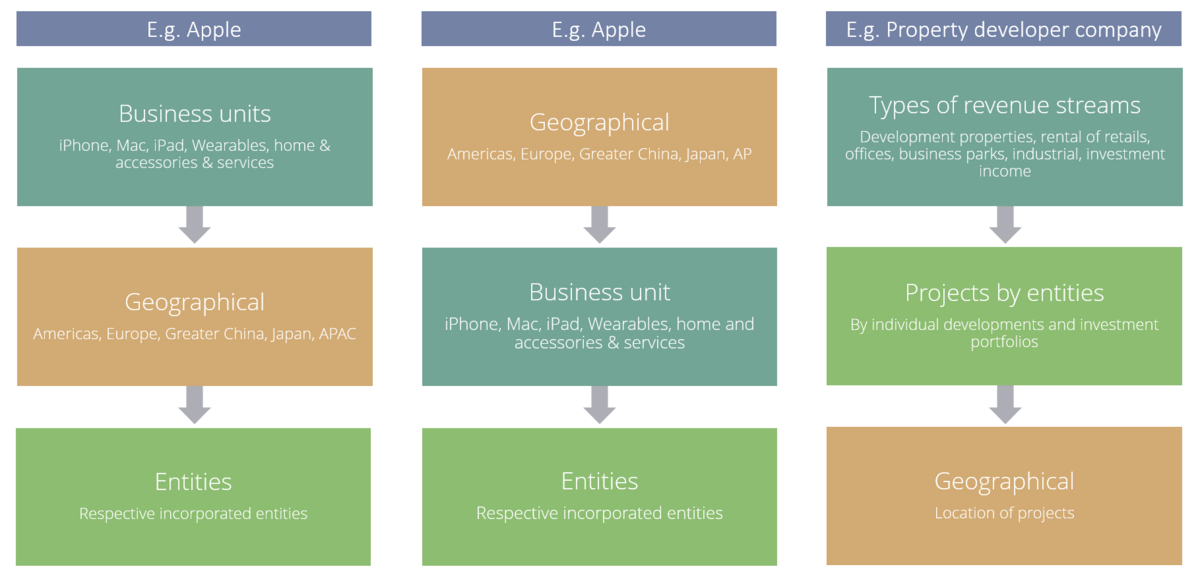

The first and most important step is to establish a logical grouping of business units into respective key segments that are reflective of the management and operations of the business. Commonly, management consolidation should accommodate different stakeholders. In our experience, large corporations typically have stakeholders in at least three hierarchy levels – CFOs, Group Financial Controllers, and Individual Group Accountants. Hence, it is crucial to ensure management consolidation is prepared efficiently to cater to different stakeholders

For example:

- Business units for Group CFOs

- Geographical for the respective region’s Financial Controllers

- Entities for Individual Group Accountants

In order to better illustrate this, Apple can group their financial data according to business unit performance for different product lines such as iPhone, Mac, and wearables for different geographical regions, and eventually how this would affect entity level performance. Additionally, Apple may also have an alternative view based on grouping financial data at a geographical level, before dissecting information down to business units and subsequently their various entities. Project-based structuring is also commonly seen in industries such as property development. In our experience, property developers can dissect their business based on revenue streams, how these are allocated to various individual developments, and subsequently their development performance based on geographical regions.

All of the information above utilizes the same source of financial data but results in varying insights when grouped differently.

Note: If the report's stakeholders request that the business units be reorganized, the report has to be reorganized as well, along with adjustments to both intra-segment and inter-segment eliminations.

Report structure

Most of the time, companies focus on the profit and loss statements that are usually a different format than the legal consolidation. However, rarely do we see management consolidation being prepared at the Balance Sheet and Cashflow level. For companies with capitalized costs relating to operating business segments, it might be helpful to have the Balance Sheet prepared to understand how costs will subsequently relate to Profit and Loss.

Note: Additional reclassifications from the general ledger accounts are required to achieve the accurate view, e.g. expenses may have to be further classified as direct or indirect.

If there are additional entries posted on individual business units that net off at the entity level, reconciling from management consolidation to legal consolidation may pose a challenge. This is because legal consolidation usually presents data by entities rather than business units.

Also, it is important to note that there may be different classifications and inter-segment eliminations due to different presentations across individual segments.

Data Preparation

Depending on how your ERP is structured, this can be an easy process or an extremely challenging one where data is required to be loaded for individual business units, followed by grouping them into the levels of the organizational hierarchy for the presentation. Subsequently, reclassifications must be performed before mapping the individual accounts to the required reporting structure.

Note:

It is important to record your data business units to allow accurate aggregation. Transactions relating to inter and intra-segments should be tagged directly to the respective entities instead of the transacting business unit. It is often insufficient and inaccurate to rely on legal consolidation eliminations for inter-segments and intra-segments elimination.

How to avoid the common pitfalls during management consolidation?

At the end of the day, the accuracy and completeness of your financial data is paramount to the ease of conducting management consolidation. In order to achieve this, there are some pointers we would suggest for your data recording process:

- Have a clear understanding of how your business is structured and have it reflected in the dimensions of your ERP, especially the business units for each entity, and correspondingly the transacting partner code.

- To facilitate the recording process, have your vendor implement automated rules if there are consistent transacting partner(s).

- Define your chart of accounts to flexibly accommodate both legal and management consolidation reporting, by ensuring that the nature of transactions for the business can be recorded specifically.

- If it is not possible, consider additional dimensions to tag key accounts, especially those relating to expenses by their nature e.g. direct or indirect.

- Reports extracted from their source system(s) to prepare management consolidation should be from the same source as legal consolidation. This can help to reduce reconciliation efforts.

- Apply the structure used in the management consolidation for budgeting and forecasting to allow benchmarking.

Your Management Consolidation Checklist

As you gear up for management consolidation, there are three key factors we would suggest keeping in mind:

Information: Management consolidation is structured to show top line, direct and indirect expenses. If each segment has different revenue streams or derived via different platforms, they should be broken down respectively. There should be a proper process established to ensure information is recorded to the required level of detail.

Presentation: Management consolidation can be presented by the business divisions or products and even by projects, whichever is most meaningful to your business. However, you should always have sufficient details included in your data to allow for further analysis such as performance by individual divisions, products, services geographical location or entity.

Measurement: Your management consolidation should also allow for a comparison of the actual results to the budget and forecast data to understand the performance of your business.

What is an easier way to do management consolidation?

At LucaNet, we help our clients with their management consolidation woes with our technological solution and consulting expertise. Our tool is designed to enable finance teams to enjoy better data management, consolidation automation, connected financial statements and custom reports. All of which will allow you to take a shortcut to a successful management consolidation process.

If you are ready to take on management consolidation, check out our solution made for your needs: